Pension Solutions

Our Pension Solutions Team partners with clients, consultants, and Loomis Sayles’ investment professionals to help deliver tailored pension strategies. We offer customized solutions using standard third-party benchmarks, spliced benchmarks, liability benchmarks, cash flow solutions, and overlays. Our collaborative approach brings together actuarial, quantitative, and credit expertise at every stage, ensuring a comprehensive strategy aligned with client objectives.

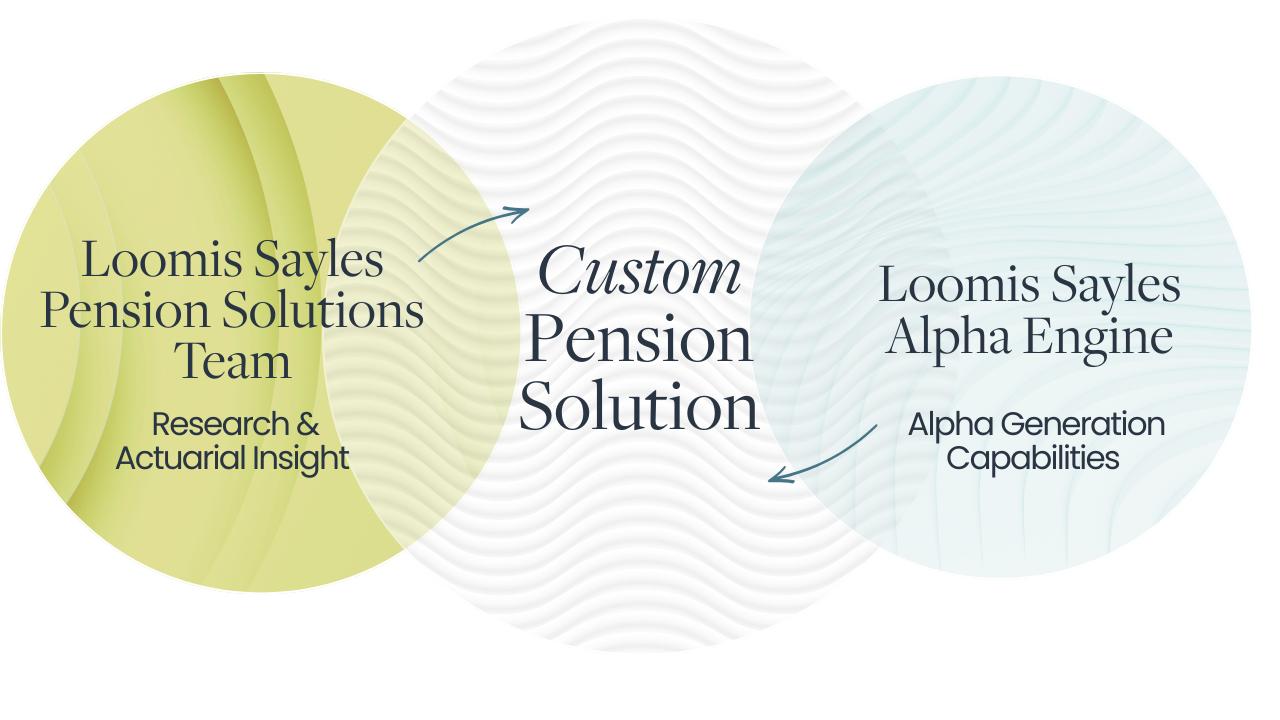

Bringing Pension Solutions to Life

Pension plan sponsors face challenges beyond managing assets. Our partnership-driven approach leverages advanced analytics through our proprietary liability-driven investments (LDI) tool kit to adapt as plans evolve. By providing total plan strategy, actionable insights, and detailed analytics, we support sponsors at every stage of a plan’s lifecycle. The integration of our Pension Solutions Team with the portfolio management team’s alpha-generating capabilities ensures that strategies are designed to deliver meaningful outcomes while meeting long-term objectives.

Our Pension Solution Credentials

By combining rigorous credit research, actuarial insight, and integrated portfolio management, our customized strategies are designed to meet the distinct liability profiles of each client.

Rigorous Credit Research

Our analysts carefully evaluate every asset to ensure alignment with liabilities and robust risk management.

Integrated Teams

Actuarial, credit, and portfolio management professionals collaborate closely to develop strategies that reflect client objectives.

Tailored Solutions for Institutions

Portfolios are customized to accommodate specific liability structures, funding goals, and risk preferences.

Ongoing Oversight

Our Pension Solutions Team continuously monitors portfolios, making adjustments as needed to respond to evolving market conditions or changes in client liabilities.

LDI AUM by Benchmark

Overview as of March 31, 2026

-

Long Corporate

$3.9 Billion AUM -

Long Credit

$6.3 Billion AUM -

Long Gov/Credit

$3.0 Billion AUM -

Spliced Benchmark

$2.1 Billion AUM -

Highly Customized

$3.1 Billion AUM -

STRIPS

500 Million AUM

We understand what matters to our LDI clients

Liability Alignment

Our customized strategies are designed to match the timing and magnitude of future liabilities, helping clients meet obligations as they come due.

Risk Management

By aligning assets with liabilities, LDI mitigates interest rate and funding risk, reducing exposure to market volatility.

Transparency

Clients gain clear insight into how portfolio assets correspond to their liability schedule, fostering confidence and alignment.

Flexibility

Pension solutions evolve as client liabilities, regulatory requirements, or funding levels change, ensuring portfolios remain responsive and relevant.

Partnership

We work closely with each client to design, monitor, and adjust strategies tailored to their specific liability objectives.

Funding Confidence

Our customized strategies aim to provide institutions with confidence that their funding targets can be met, even amidst changing market conditions.

Recent Thought Leadership

How does your asset manager stack up? Measuring performance with Benchmark Snapping.

Every client has distinct objectives, requiring portfolios designed to achieve specific goals. At Loomis Sayles, we want to redefine how institutions assess[…]

An LDI Playbook for 2025

As we head into 2025, corporate pensions continue to sit in a comfortable position relative to history.

Higher for Longer: A Window of Opportunity for Cash Flow Generating Strategies?

We think it is an opportune time to consider cash flow generating strategies that can capitalize on the currently higher yield levels[…]

Interested in Loomis Sayles Pension Solutions?

Our team is ready to talk custom solutions–reach out and find your investment partner today.

Justin Teman, CFA, ASA

Head, Institutional Advisory Group

Important Disclosure

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Investment decisions should consider the individual circumstances of the particular investor. Any opinions or forecasts contained herein, reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Information, including that obtained from outside sources, is believed to be correct, but we cannot guarantee its accuracy. This information is subject to change at any time without notice.

Investment vehicles may not be available to all investors and are subject to eligibility.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

Market conditions are extremely fluid and change frequently.

Past performance is no guarantee of future results.