Author

July 2026 Investment Outlook

We believe the expansion phase of the global credit cycle will continue through 2026, backed by decent economic growth and stable labor markets.

There is potential for inflation to decline across developed and emerging market economies through the latter part of this year. Oil prices have come down significantly since the breakout of the US-Iran war, which should relieve much of the pressure on headline inflation.

Corporate profit growth, a dominant cyclical driver, has been booming globally. Artificial intelligence (AI) and related data center buildouts are boosting activity beyond the technology sector to industrials and utilities. The associated pipeline of capital expenditures will be massive. We believe AI will continue to drive economic and profit growth, especially within the United States and Asia.

Investment Themes

Our take on macro drivers and major asset classes at a glance.

Macroeconomic Drivers

Economic growth and labor markets are in a good place throughout most of the world, but sticky inflation remains a concern.

Corporate Credit

Measures of risk premium across global credit markets suggest valuations are a bit elevated relative to history, but for good reason.

Government Debt & Policy

Developed market interest rates are still near their highest levels of this cycle. We expect rates to slide lower slowly as inflation finds its way toward central bank targets.

Currencies

We see opportunities in relatively higher-yielding local-currency fixed income markets outside the US.

Global Equities

Strong bottom-up fundamentals should propel the global equity rally through year-end and into 2027. Most indices are on pace to deliver double-digit earnings growth this year.

Potential Risks

Our investment outlook is predominantly bright, but there are scenarios where positive market trends could be disrupted. Rising inflation and rate hikes outside the US could spark higher long-term interest rates.

Macroeconomic Drivers

Economic growth and labor markets are in a good place throughout most of the world, but sticky inflation remains a concern.

- We do not believe a significant rally across fixed income markets is likely to take hold near term.

- However, we do believe interest rate volatility across the curve should remain subdued, allowing investors to earn their yield.

- In our view, central bankers no longer have an easing bias, but we are not concerned about cycles of aggressive rate hikes.

- We could see single rate hikes in the euro zone, UK and perhaps Japan by year-end, but nothing more.

- Federal Reserve (Fed) rate cuts are likely on hold through year-end, but could resume in the first quarter of 2027 if inflation cooperates.

- Emerging market central banks could strike a less hawkish tone as the year progresses, especially if oil market volatility remains subdued.

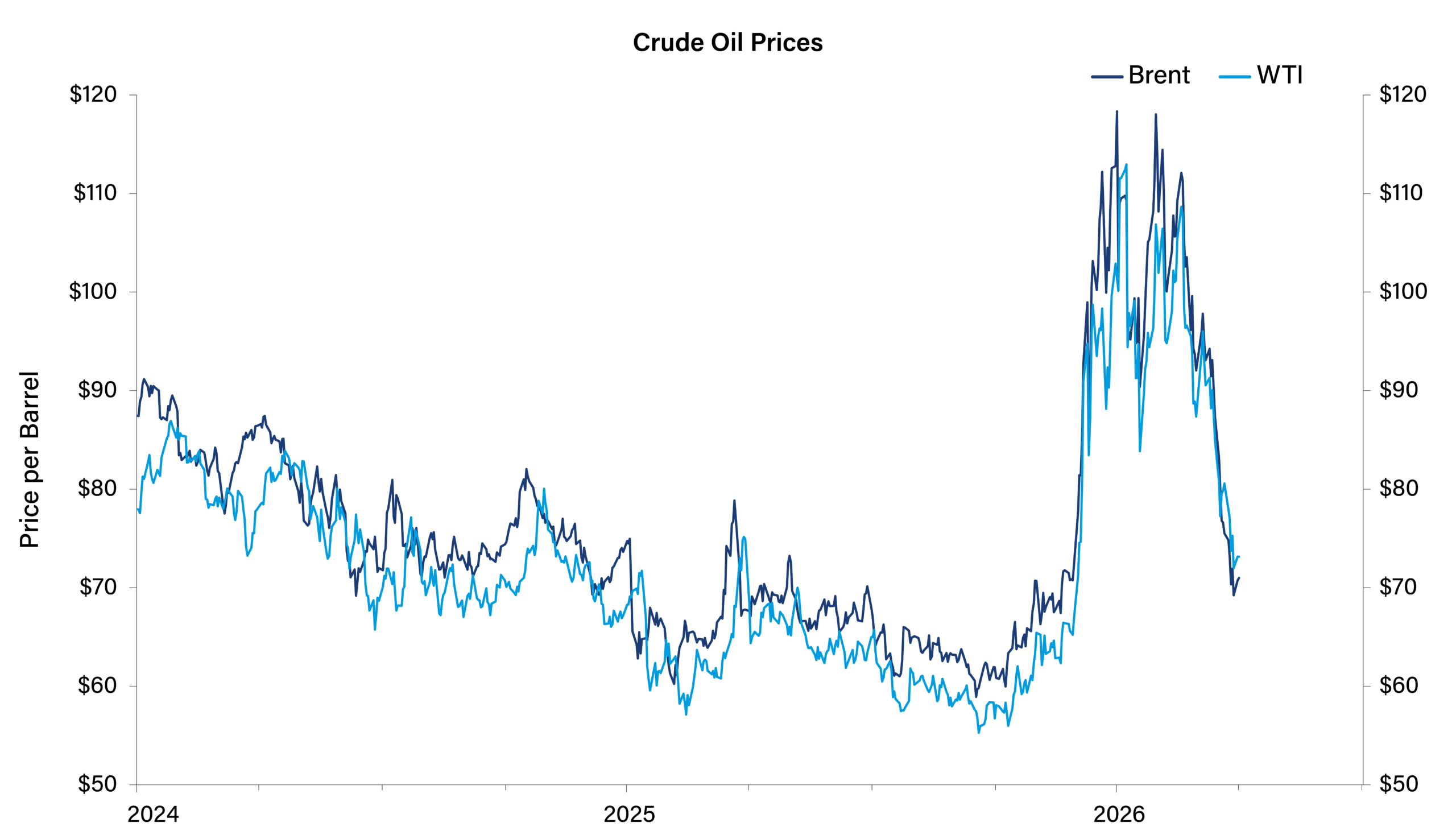

- A finalized deal between the US and Iran could reverse oil shortages and global supply chain disruptions, albeit over several weeks.

Crude oil prices would have to spike and remain high for consumers to alter their spending patterns.

While we expect some geopolitical risk premium to keep oil above pre-war levels, a significant decline has already occurred.

Source: Bloomberg, rolling active monthly crude oil futures contracts, as of June 30, 2026. West Texas Intermediate (WTI) is a high-quality, easily

refined grade of crude oil that serves as the primary benchmark for oil pricing in North America. Brent is the primary international benchmark for

the majority of oil pricing.

Corporate Credit

Measures of risk premium across global credit markets suggest valuations are a bit elevated relative to history, but for good reason.

- Global interest rates have been normalizing since the start of the current expansion, and remain at levels materially higher than the post-Global-Financial-Crisis (GFC) recovery period.

- Corporate credit benchmarks offer impressive income opportunities at present. We expect the asset class to deliver mid-single-digit total returns even if credit spreads do not tighten.

- Higher-credit-quality indices are yielding between 3% and 5% annually. We think assuming credit risk higher than that of high-grade benchmarks could produce equity-like total returns.

- Bottom-up fundamentals, like profit margins, earnings growth and leverage, are in very good shape broadly.

- Domestic large-cap companies, which are a decent proxy for the US investment grade credit market, are seeing profit margins expand to all-time highs.

- Small cap companies within the US are a decent proxy for the domestic high yield credit market. Bloomberg bottom-up consensus earnings estimates for the Russell 2000® Index are projecting 35% earnings growth in 2026.

- We’re monitoring risk in the private credit market, and do not see signs of systemic risk given expectations for a robust economic backdrop.

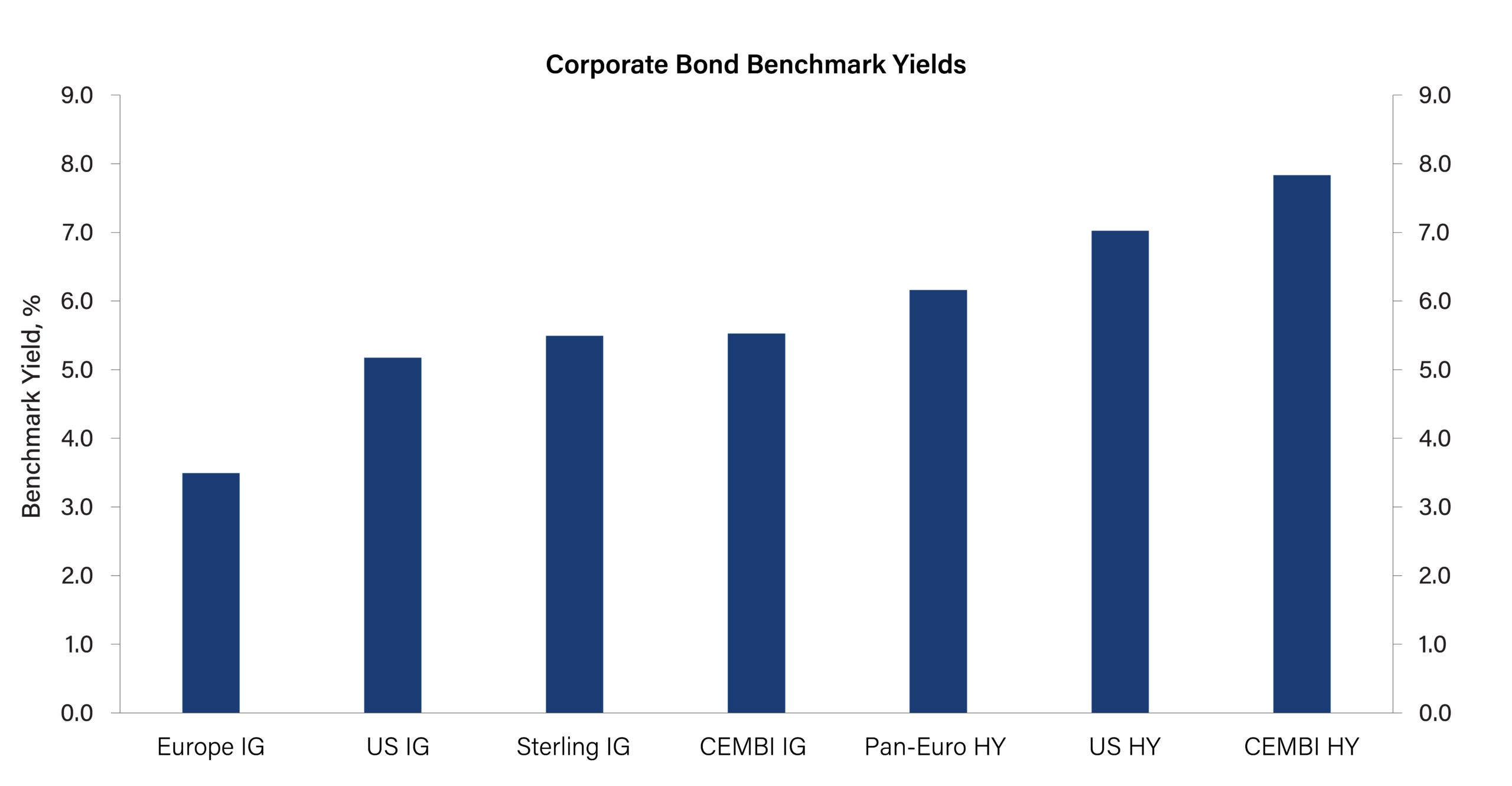

Our credit research analysts are able to find potential risk/reward opportunities within credit markets that typically have higher yields than the investment grade Bloomberg US Aggregate Corporate Index.

Moving out on the quality spectrum to high yield credit could offer significant total returns.

Source: Bloomberg, JP Morgan as of June 16, 2026. IG: Investment Grade. HY: High Yield. CEMBI: Corporate Emerging Markets Bond Index.

The chart presented above is shown for illustrative purposes only.

Government Debt & Policy

Developed market interest rates are still near their highest levels of this cycle. We expect rates to slide lower slowly as inflation finds its way toward central bank targets.

- Government debt burdens are large but manageable. Over the next six to 12 months, we believe cyclical factors like inflation and economic activity will dictate the range for bond yields.

- Economic tailwinds, like the AI capital expenditure spending cycle, are likely to keep driving growth, but that does not mean inflation has to be sticky.

- We believe yields across the developed world have peaked or are close to peaking. That said, significant bond rallies are not part of our near-term outlook.

- We expect (and would welcome) a slow drift lower in inflation. An abrupt drop would likely signal a deeper issue related to demand challenges in the economy.

- The next move for interest rates and inflation is lower, but the process is likely to take quarters rather than months.

- We anticipate the US 10-year yield will trade between 4.0% and 4.25% as we enter 2027.

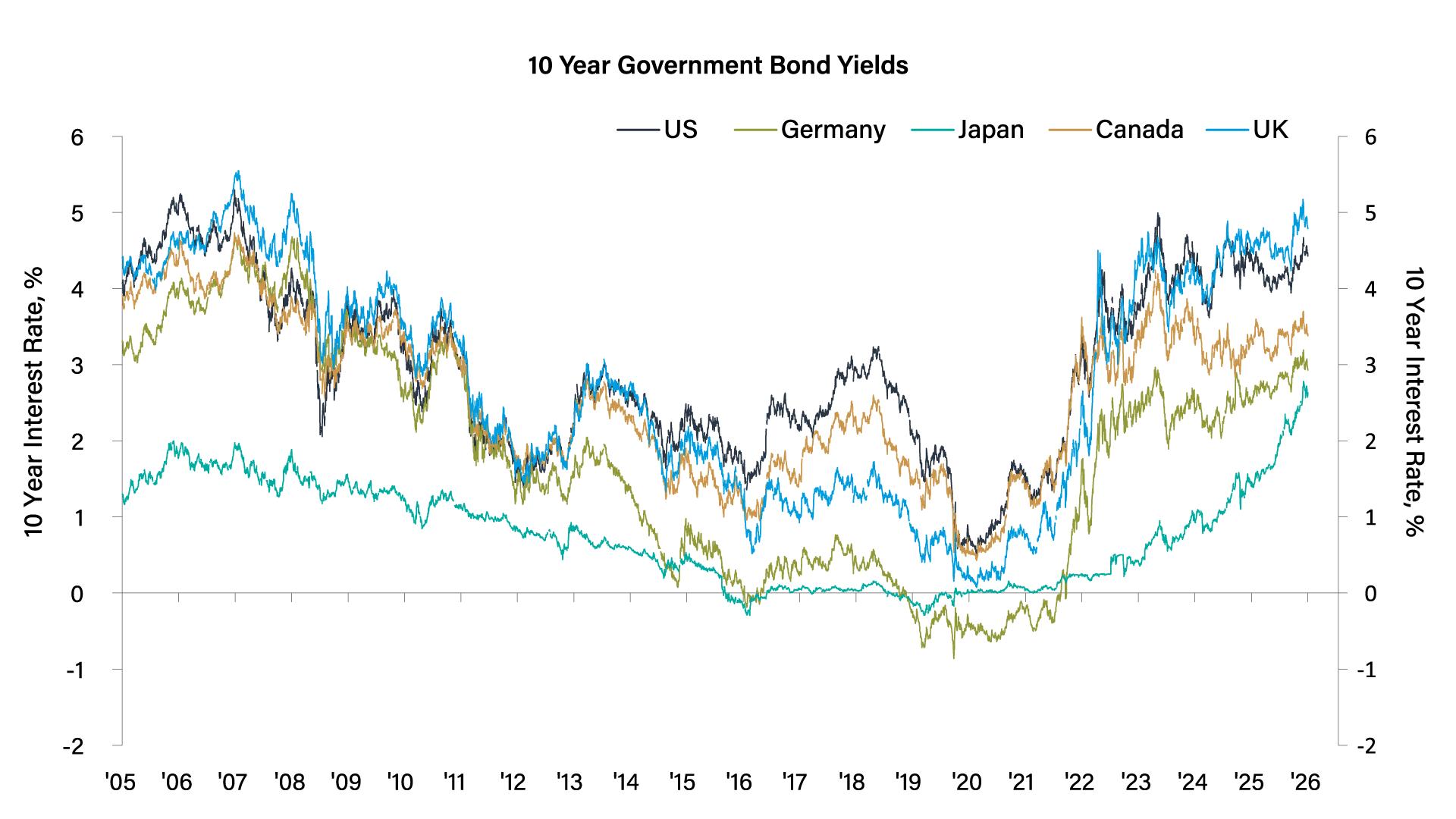

High-quality government bonds should perform well as a hedge in the next downturn, but we expect such an event to be far out on the horizon.

Most high-grade government bonds should bounce within a fairly tight range for the next two quarters. Japan is likely nearing a major peak.

Source: Bloomberg as of June 16, 2026.

The chart presented above is shown for illustrative purposes only. Past performance is no guarantee of future results.

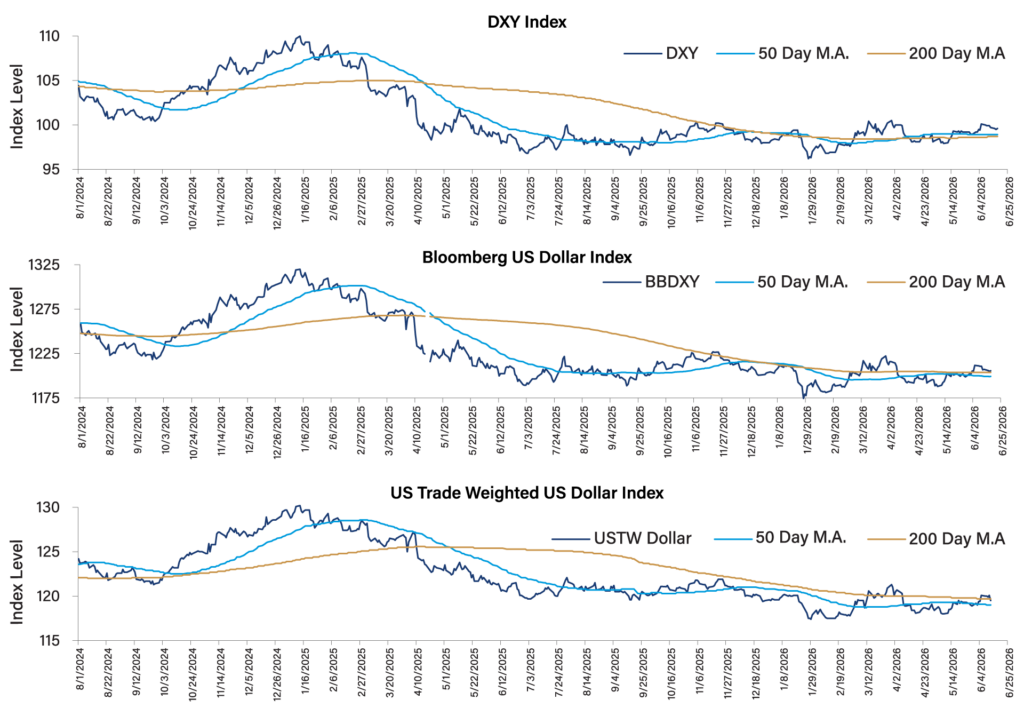

Currencies

We see opportunities in relatively higher-yielding local-currency fixed income markets outside the US.

- Non-US-dollar assets can perform well as the global expansion progresses. A sustained ceasefire in the Middle East is increasing our optimistic view.

- Our preferred countries for local-currency exposure include Brazil, Hungary, Mexico and Colombia. Their attractive yields and decent underlying economic conditions stand out.

- We have a selective approach to owning non-dollar assets. We do not believe the US dollar is going significantly lower from here, even if rate cuts are slowly priced back into market expectations.

- The US Dollar Index (DXY) has been trading within a 4% range for the better part of one year. We anticipate some weakness in the quarters ahead, but see downside capped at just a few percentage points.

- We expect risk appetite to remain strong. In such environments, foreign currencies tend to perform well.

The US Dollar Index could trade down toward the bottom of its one-year range if market conviction in rate hikes begins to wobble.

The dollar indices have not done much over the past year, but we are identifying individual currency opportunities beneath the surface.

Source: Bloomberg, as of June 16, 2026. Used with permission from Bloomberg Finance L.P.

Global Equities

Strong bottom-up fundamentals should propel the global equity rally through year-end and into 2027. Most indices are on pace to deliver double-digit earnings growth this year.

- Earnings growth rather than multiple expansion has predominantly fueled recent equity market gains across the globe. This trend is likely to continue.

- AI-related capital expenditures are driving earnings with far-reaching multi-sector implications. It’s a powerful trend that remains intact.

- The information technology and communication services sectors of the S&P 500 Index are leading the pack in terms of growth. However, several other sectors delivered double-digit growth for the first quarter. Healthcare was the only sector that showed a modest earnings contraction year over year.

- The MSCI All Country World Index (ACWI) excluding the US, looks set to deliver 25% earnings growth this year. The S&P 500 should see a 20%-or-better increase, while small-cap Russell 2000 earnings could rise more than 30%.

- Most markets have been consolidating rapid gains since March. We believe there is more upside ahead, particularly if war in the Middle East winds down.

Technology and AI-related equities are outperforming, and broad US stock market breadth is in decent shape.

As the market makes new highs, we are seeing improving rally participation.

Past performance is no guarantee of future results.

Source: Bloomberg, as of June 16, 2026.

Potential Risks

Our investment outlook is predominantly bright, but there are scenarios where positive market trends could be disrupted. Rising inflation and rate hikes outside the US could spark higher long-term interest rates.

- Global central bank tightening is a risk that could push yield curves higher across the world.

- Oil prices tumbled recently, but renewed military tensions in the Middle East could send prices higher.

- A return of higher oil prices would likely propel inflation upward for longer, which could put renewed pressure on central banks to act.

- Optimism surrounding the massive AI-driven capital expenditure cycle is running hot. Major setbacks would likely disappoint markets and slow future economic and earnings growth.

- Technology and AI-related industries are largely responsible for the upward revisions to 2026 consensus earnings growth. At some point, expectations may prove too rosy.

- S&P 500 consensus earnings growth for 2026 is a significant, but likely achievable, 24%. Estimates of 16% and 12.5% for 2027 and 2028 respectively are starting to look questionable given such strong expectations to conclude 2026.

- Earnings have been a key driver keeping the credit cycle in expansion. Continued strong earnings growth will be vital for maintaining positive market momentum.

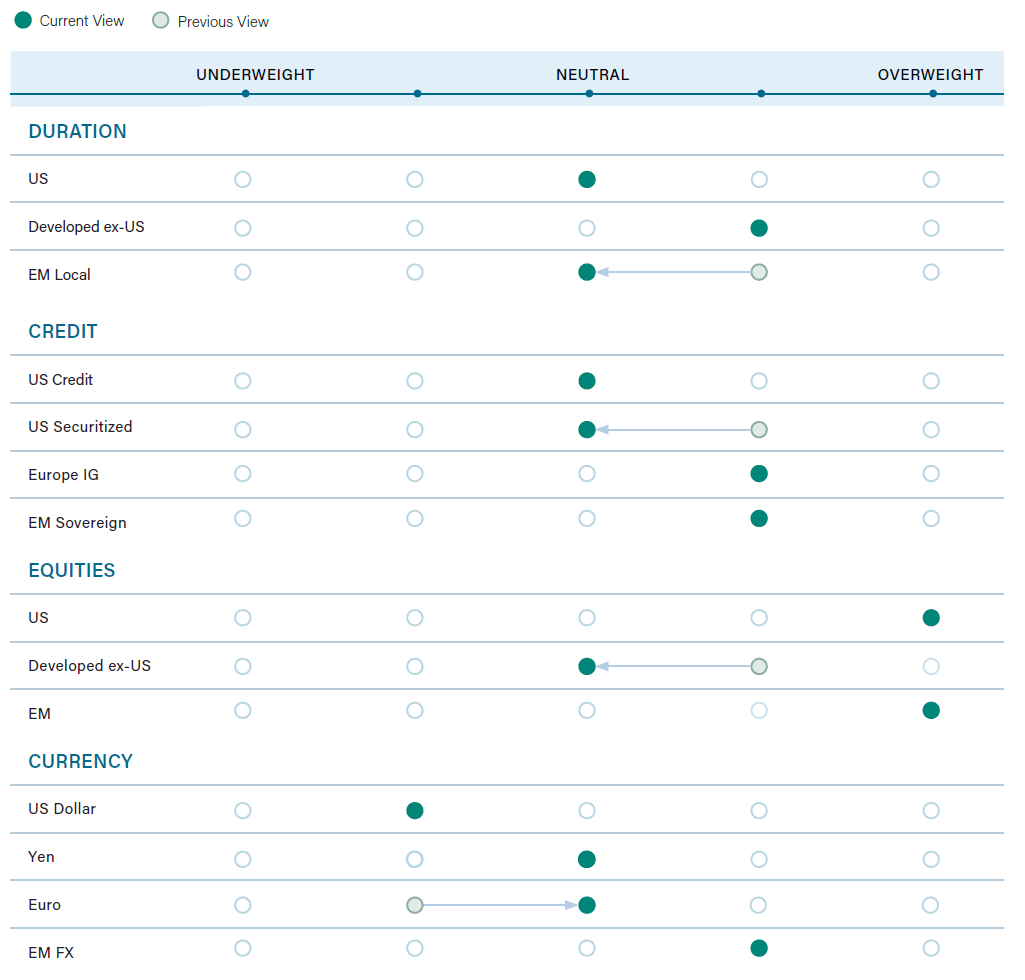

Asset Class Outlook

With macro tailwinds already priced into the market, valuations are not particularly compelling. Investors should be

ready to act when volatility inevitably spikes.

*EM FX = Emerging Markets Foreign Exchange

Disclosure

The S&P 500® Index is a widely recognized measure of US stock market performance. It is an unmanaged index of 500 common stocks chosen for market size, liquidity, and industry group representation, among other factors. It also measures the performance of the large-cap segment of the US equities market.

It is not possible to directly invest in an index.

Some or all of the information on the charts may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

Past performance is no guarantee of future results.

Market conditions are extremely fluid and change frequently.

Any investment that has the possibility for profits also as the possibility of losses, including the loss of principal.

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein, reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual, or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but we cannot guarantee its accuracy. This information is subject to change at any time without notice

KEY RISKS: Inflation Risk, Fixed Income Risk, Systemic Risk, Currency Risk, and Market Risk.

8989591.1.1

Author