Unlocking Value in Private Credit: Inside Loomis Sayles’ Integrated Approach

Loomis Sayles anticipates that the continued expansion of the private credit market will unlock compelling opportunities for fixed income investors.

In alignment with this strategic outlook, the firm has built a dedicated Private Credit Team and employs cross-functional deal teams that leverage Loomis Sayles’ broad credit capabilities to identify and analyze transactions that they believe represent the most attractive opportunities across the public/private fixed income spectrum. This approach harnesses Loomis Sayles’ extensive credit expertise to source and evaluate private credit opportunities across both multi-asset public/private portfolios and dedicated private credit mandates.

Key Takeaways

- Private credit generally offers higher yields and structural protections relative to public bonds, qualities that may help it deliver attractive risk-adjusted return potential.

- Loomis Sayles’ specialized Private Credit Team works closely with the firm’s public markets portfolio managers and research analysts to evaluate opportunities and assess relative value across public and private fixed income markets.

- This integrated approach ensures that each private credit investment benefits from the full breadth of

Loomis Sayles’ market knowledge, analytical depth and specialized legal insight. - As private credit evolves, we continue to emphasize strong market access, analytical rigor and potential yield advantage coupled with structural protection to build resilient portfolios for institutional and retail investors.

An Experienced Team

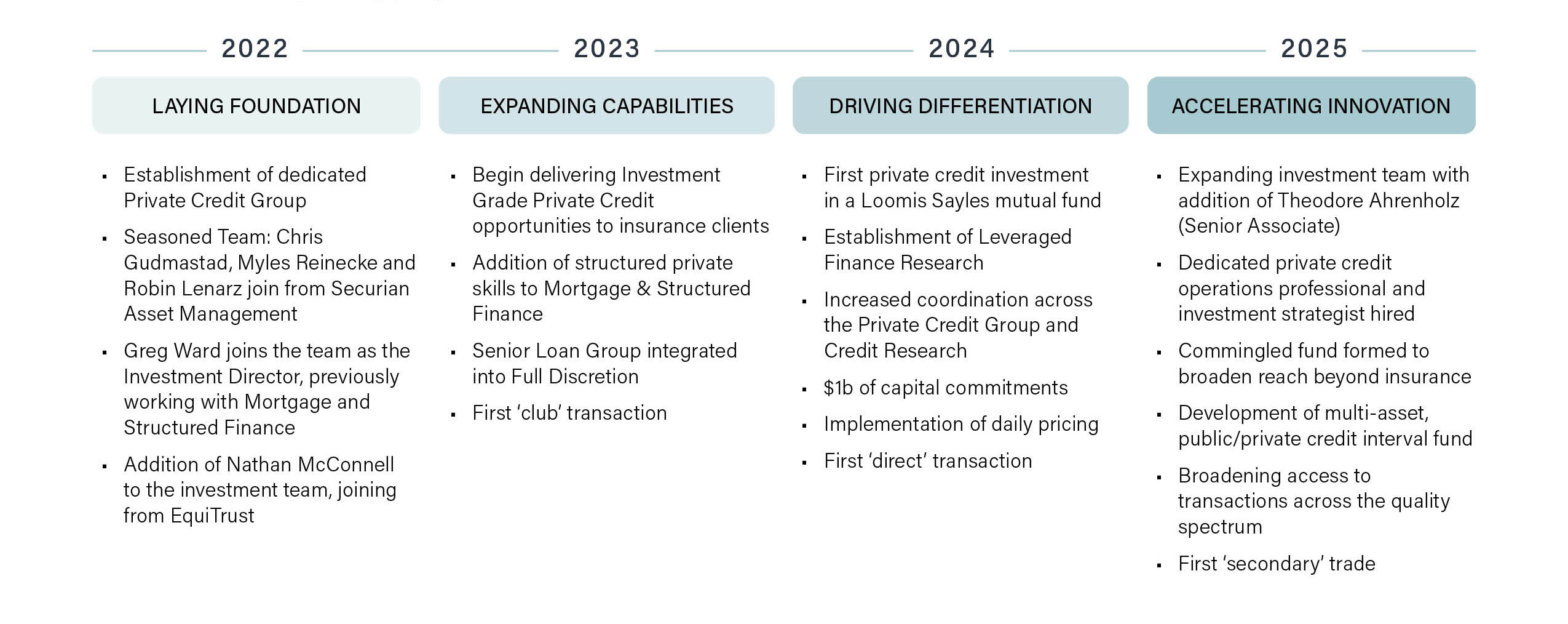

Chris Gudmastad joined Loomis Sayles in early 2022, drawing on nearly two decades of private credit experience to develop and lead the firm’s integrated private credit platform. Two additional hires in 2022 rounded out the initial team: Myles Reinecke, who joined as a Portfolio Manager and Managing Director with more than a decade of experience, and Robin Lenarz, a seasoned transaction attorney dedicated to supporting the team’s investment activities.

This core trio, who worked together previously at Securian Asset Management, brought a high degree of continuity in investment philosophy and process. As of October 2025, the Private Credit Team has grown to eight professionals and encompasses a broad spectrum of private markets investing and operational expertise, positioning Loomis Sayles to potentially capitalize on the evolving private credit landscape with depth and agility.

An Integrated, Multi-Disciplinary Approach

The Loomis Sayles Private Credit Team is strengthened by cross-functional deal teams that integrate insights from across the firm.

Dedicated private credit analysts work closely with public markets portfolio managers and research analysts, including the firm’s 59-member Credit Research Department, 20-member Mortgage and Structured Finance (MSF) Team, and Loomis Sayles’ Macro and Sovereign Research Groups to evaluate each opportunity with the benefit of multiple viewpoints.

For corporate-issued private credit transactions, the assigned private credit analyst partners with the relevant public markets credit analyst and the firm’s dedicated private assets legal counsel to form a tailored deal team. In the case of asset-based finance transactions, the Private Credit Team collaborates extensively with the MSF Team, who bring deep expertise across the consumer, commercial and real estate sectors within the securitized universe. This integrated approach seeks to ensure that each private credit investment benefits from the full breadth of Loomis Sayles’ market knowledge, analytical depth, and specialized legal insight, enhancing the team’s ability to identify and execute on attractive investment opportunities.

Sourcing Investment Opportunities

Loomis Sayles’ Private Credit Team benefits from a robust, diversified sourcing network built on deep relationships with issuers, bankers, private credit managers and other market participants.

These connections are the primary gateway to a steady pipeline of private credit opportunities across a wide range of sectors—giving the team privileged access to deals that may not be broadly marketed.

The team has experience underwriting and investing across multiple origination channels, including syndicated, club, direct and secondary transactions. This breadth of sourcing affords greater selectivity and flexibility in portfolio construction.

Importantly for investors, the team views the private credit universe through three distinct opportunity sets:

- Corporate Credit

- Asset-Based Finance (including consumer, commercial and specialty finance)

- Real Assets (including real estate, infrastructure and project finance)

Each category offers investment grade and high yield opportunities, enabling the team to tailor exposures to meet specific risk-return objectives. Through expansive reach and multi-channel sourcing capability position, Loomis Sayles seeks to uncover differentiated opportunities that can enhance portfolio yield, diversification and downside protection.

Private Credit’s Powerful Paradox

We believe private credit presents investors an opportunity to enhance yield without taking on higher credit risk

because of two key features:

- Incremental Yield: Private credit enjoys a well-established liquidity premium, which compensates investors for holding less tradable assets, and a complexity premium, reflecting customized solutions for bespoke or structurally intricate transactions.

- Structural Advantages: Transactions often include lender-friendly protections, such as covenants and customized terms, which can help mitigate downside risk and preserve capital in adverse scenarios.

This combination of higher income potential and enhanced downside mitigants creates a powerful paradox: investors may achieve stronger risk-adjusted return potential in private credit than in traditional public credit markets. It may also be an attractive option for investors seeking differentiated sources of return and resilience in volatile environments.

Institutional investors—like insurance companies and pension funds—have long been drawn to private credit because they often seek stable, predictable cash flows to match liabilities, and private credit’s risk/return profile is generally well-suited to those objectives. We believe the asset class can play a similar role for retail investors seeking to improve risk-adjusted return potential and strengthening portfolio resilience.

Loomis Sayles’ Private Credit Team process follows a disciplined five-step approach:

- Deal Origination: The team sources transactions through long-standing relationships with banks, issuers and asset

management peers—ensuring consistent access to high-quality opportunities. - Credit Underwriting: A cross-functional deal team conducts deep analysis, including management engagement,

financial modeling, stress testing and relative value assessment. Each deal is assigned internal ratings for credit risk,

recovery potential and liquidity. - Legal & Structure Review: Specialized legal staff and external counsel assess jurisdictional and structural elements,

negotiating covenant enhancements to strengthen downside protection. - Decision Making & Portfolio Construction: Selectively invest in the best bottom-up opportunities with position sizing

based on risk-versus-return and individual account parameters. - Surveillance & Risk Management: The team actively monitors portfolio holdings to track financial health and covenant

compliance using internal watchlists and rating triggers to manage risk proactively.

The private credit market is evolving and the asset class is becoming a strategic allocation for many fixed income investors.

With a seasoned team, a disciplined investment process, and deep integration across Loomis Sayles’ credit research and structured finance capabilities, we believe the private credit platform is well-positioned to deliver differentiated opportunities and strong risk-adjusted return potential.

PRIVATE CREDIT EVOLUTION

Focused on making steady progress as scale is built

8161220.2.1

This material is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the

subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations

may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. This information

is subject to change at any time without notice.

Past performance is no guarantee of future results.

Important Disclosures

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein, reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual, or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Diversification does not ensure a profit or guarantee against a loss.

Market conditions are extremely fluid and change frequently.

Commodity, interest and derivative trading involves substantial risk of loss.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

There is no guarantee that the investment objective will be realized or that the strategy will generate positive or excess return.

8683973.1.1

Meet the Authors