Municipal Market Update

2nd Quarter 2026

Economy & Rates

- The US Treasury interest rates generally moved higher during the second quarter. The largest increase in Treasury yields occurred in the 2-3 year portion of the yield curve, as the market priced in “higher for longer” and potential tightening implications for Fed policy rates. This dynamic reflected continued economic resilience, persistent inflation readings, the inflationary impact of the Iran conflict—particularly upon energy costs—and ongoing concerns about longer-term inflation trends and fiscal deficits.

- The Federal Reserve (Fed) maintained a pause in rate cuts at the June Federal Open Market Committee (FOMC) meeting. New Fed Chairman Kevin Warsh grappled with dissenting views within the Committee and issued a post-meeting public statement that was notably terse compared to those of his predecessor. Forward guidance from Warsh was limited but the Committee reiterated its commitment to eventually returning inflation to a 2% target level. The market is no longer forecasting a Fed rate cut during the remainder of 2026 with the possibility of a rate hike this year now on the table.

- The Treasury yield curve remained positively sloped, with front-end yields anchored by Fed policy and longer-term yields influenced by persistent inflation expectations and fiscal considerations. The 2-year/10-year yield spread tightened somewhat in the second quarter, from around 50 basis points (bps) to around 30 bps at quarter end, as shorter 2-3 year tenors reacted more directly to the change from Fed easing to tightening expectations, while the longer end is still reflecting expectations for inflation to moderate over time.

- The outlook for the US economy, in our view, remains constructive. We expect positive GDP growth of approximately 2%, driven by resilient consumer spending, solid corporate investment (including AI-related capital expenditures), and supportive fiscal programs.

- As of 6/26/2026, Loomis Sayles’ Macro Strategies team assigned a 55% probability to an “Expansion Resilient” macro scenario as their base case, which forecasts that growth is likely to persist with a boost from fiscal programs, artificial intelligence productivity gains, strong corporate earnings growth, and a stable but cooling labor market. “Economic Boom” (marked by a more resilient economic growth trend, an upward bias to yields, and Fed rate hikes in 2027) is assigned a 35% likelihood, and “Downturn” (essentially a mild recession scenario marked by a pullback in consumer spending, negative S&P 500 earnings growth, and a more accommodative Fed) is assigned a 10% likelihood.

Municipal Market Performance

- Contrary to the Treasury curve, municipal (muni) yields fell in the second quarter. The yield rally was the strongest around the 20-year part of the curve, where yields fell 45 bps. Yields in the 20-30 year tenors rallied 30-40 bps, with more muted rate declines at the 10-year (-19 bps) and 5-year (-5 bps) marks. The net effect is a lower and flatter yield curve than was seen at the beginning of the quarter.

- The contrasting response of the muni yield curve relative to the Treasury curve in Q2 had several likely contributors. We believe Treasurys sold off (curve rose) largely due to market expectations for a more hawkish Fed response in reaction to persistent inflation expectations, which in turn is fueled by the resilient economy. Conversely, munis rallied (curve lowered) due to seasonally strong demand for munis into the summer months as well as a persistent retail bid for munis driven by the compelling tax-adjusted yields offered by the asset class.

- Municipal bond credit spreads were a mixed bag in the second quarter. Overall, spreads inside of 10 years were little changed. This is the part of the curve where the majority of retail dollars flow; thus, the strong retail bid provided support and stabilization. Beyond 10 years, we did observe a modest amount of spread widening, where some of the effects which also impacted Treasurys (persistent inflation, hawkish Fed tone) were felt more directly.

- The net effect of the yield curve falling, credit spreads being relatively stable, and a still elevated level of carry was a solidly positive return for the Bloomberg Municipal Bond Index, which posted a 2.50% return in Q2. While total return in Q2 was positive across all tenors, it did vary notably at different points on the curve. At the 20-year mark returns for the quarter were just north of 4%, aided by the largest yield declines and a high level of embedded carry. Returns declined commensurate with more muted rate movements and carry shorter on the curve, with positive returns of around 2% at the 10-year mark and 1% around the 5-year mark.

Source: Bloomberg

Returns for multi-year periods are annualized. Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Past market performance is no guarantee of future results.

- From a credit quality perspective, lower quality investment grade tax-exempt munis (BBB and A-rated) posted slightly stronger performance in the second quarter, and revenue backed bonds outperformed General Obligation bonds.

- All sectors of the investment grade tax-exempt muni market posted positive returns for the quarter. Among our focus sectors, hospitals fared the best, returning 3.10% in Q2, whereas electric power utilities posted a relatively weaker return of 2.39%.

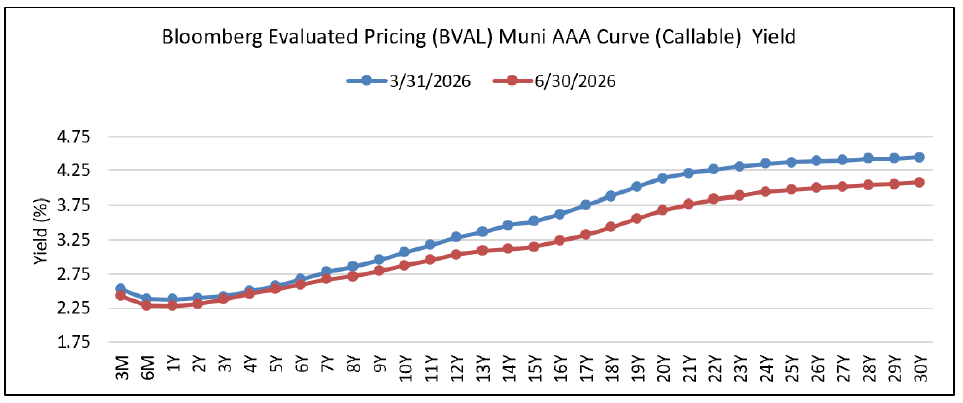

- At the end of the second quarter, the muni curve maintained a generally normal, upward-sloping shape, aside from a bit of a “hook” inside of six months where yields were elevated in correlation with the Fed funds rate. Although the curve flattened a bit in Q2, AAA-rated bonds on the long end of the curve still offered4%+ tax-exempt yields.

Source: Bloomberg as of 6/30/26

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Past market performance is no guarantee of future results.

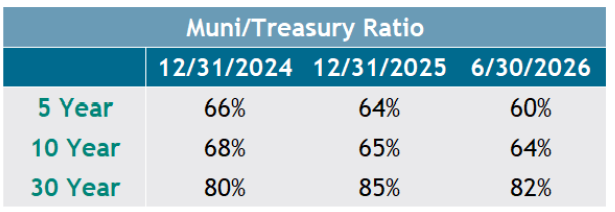

- Muni valuations, as measured by the muni-to-treasury ratio, richened (declined) in the second quarter after cheapening during the first quarter. This makes sense given the different outcomes for the Treasury (rates rose) and muni (rates fell) yield curves in the quarter, against a backdrop of relatively stable muni credit spreads. As mentioned, munis also enjoyed a persistently strong retail bid which helped to insulate the market from some of the macroeconomic pressures felt by Treasurys. As a result, the 5-year muni-to-treasury ratio now appears rich by historical standards, with the 10-year and 30-year ratios appearing “somewhat rich” in our opinion.

Source: Bloomberg

Returns for multi-year periods are annualized. Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Past market performance is no guarantee of future results.

Muni Supply & Demand

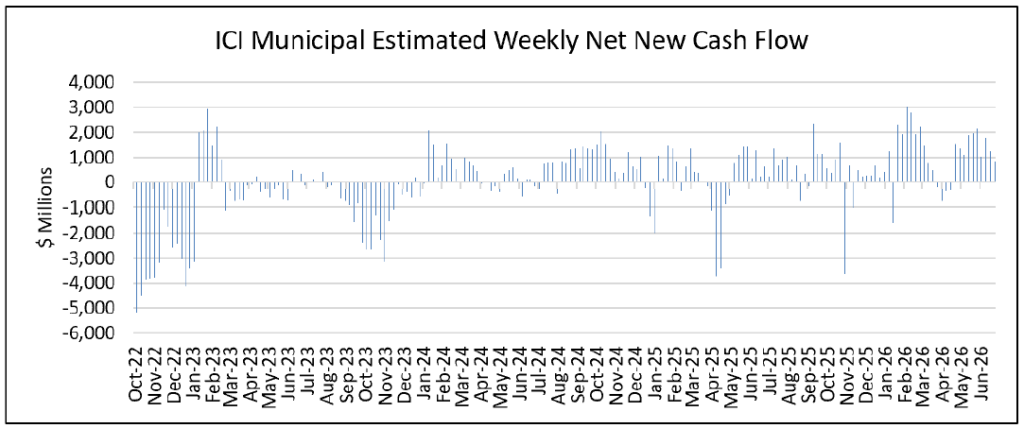

- The flow of investor money into municipals demonstrated a positive trend in Q2, with weekly muni mutual fund flows remaining primarily positive and with separately managed account (SMA) and exchange-traded fund (ETF)demand remaining robust as well. Mutual fund net inflows totaled approximately $13-14 billion in the quarter.

Source: Bloomberg, as of 6/30/2026.

Past market performance is no guarantee of future results.

- New muni bond supply expectations remain strong, given increased project costs and less supportive Fiscal Policy. New issuance of muni bonds year-to-date tracked approximately 11-12% ahead of the same period in 2025. We expect strong new issuance to continue, albeit potentially at a slightly lower pace than 2025’s record pace. New issuance continues to be fueled by inflationary effects (which increase municipal project costs) and decreased federal support for state and local entities, which could induce new borrowing needs and spur incremental new issuance. However, an upward trend in interest rates (i.e., borrowing costs) could start to taper supply.

- From a technical perspective, seasonal flows from bond coupons and maturities entered a relatively strong time of year in June, which should persist through the month of August. While this cycle is a known annual event and just one factor in what moves the muni market, stronger seasonals can help to create an additional demand tailwind in an environment of already strong retail demand for munis.

Outlook

The following conditions underpin our moderate outlook for the municipal market:

- Elevated absolute yields and a somewhat steep muni yield curve offer an opportunity for attractive carry and rolldown.

- On a probability-adjusted basis, we forecast lower interest rates during the next year, but we note the increasing likelihood of an Economic Boom scenario,which could push rates higher from current levels.

- On a “tax equivalent” basis, munis may provide a compelling alternative to other investment grade credit asset classes, particularly for high tax bracket investors.

- We expect demand from retail investors in mutual funds, ETFs and separately managed accounts to continue absorbing the heavy pace of new issuance and bring balance to the muni market. Additionally, as Q2 ended, we have entered a period of seasonally stronger reinvestment flows, which could further aid in the absorption of new issuance.

- Credit spreads on the front end of the curve are close to fair value in our opinion, while longer on the curve look slightly rich relative to historical averages.

- While credit conditions in several muni sectors are being impacted by Fed policy headwinds, an overall upbeat macroeconomic tone has provided stability to the credit environment.

- Valuations, especially across the shorter tenors, appear relatively rich by historical standards.

- The risks that challenge our forecasts include Fed policy uncertainties that could impact the credit fundamentals of weaker quality muni issuers, the impact of inflation which could affect the extent and timing of future Fed rate decisions, and the potential for a persistently strong economy which pressures long-term rates higher.

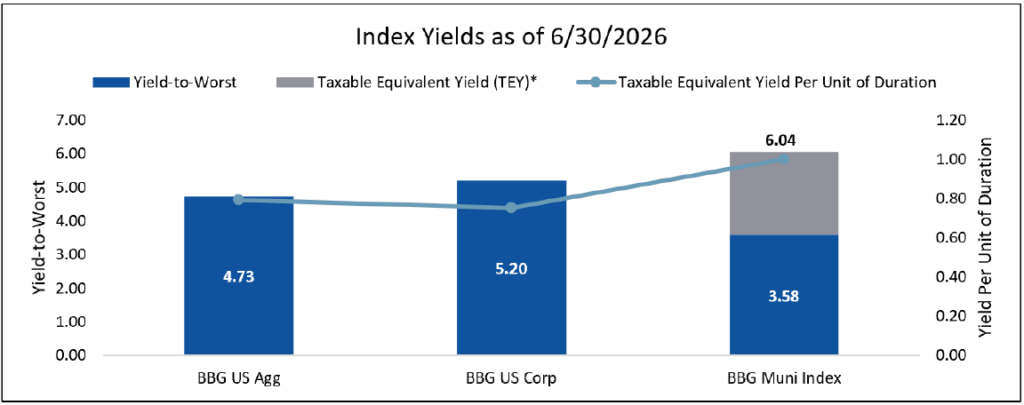

The Bloomberg Municipal Bond Index sported a 3.58% yield at quarter-end, which equates to a 6.04% Taxable Equivalent Yield (using an effective tax rate of 40.8%). We believe this represents reasonable value -and a possible entry point -relative to the Bloomberg US Corporate Bond Index and the Bloomberg US Aggregate Index.

*The taxable equivalent yield is calculated using an effective tax rate of 40.8% which includes the 37.0% top federal marginal income tax rate and the 3.8% Net Investment Income Tax to fund Medicare. Source: Loomis Sayles and Bloomberg as of 3/31/2026. Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This material is not intended to provide tax, legal, insurance, or investment advice. Please seek appropriate professional expertise for your needs. Past market performance is no guarantee of future results.

IMPORTANT DISCLSOURES

Past performance is no guarantee of future results.

Market conditions are extremely fluid and change frequently.

Diversification does not ensure a profit or guarantee against a loss.

Any investment that has the possibility for profits also as the possibility of losses, including the loss of principal.

This material is not intended to provide tax, legal, insurance, or investment advice. Please seek appropriate professional expertise for your needs.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein, reflect the subjective judgments and assumptions of the authors only, and do not necessarily reflect the viewsof Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual, orexpected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but we cannot guarantee its accuracy. This information is subject to change at any time without notice.

For Investment professional use only. Not for further distribution.

9005465.1.1

Author