Is China’s Renminbi the New “Safe Haven” Currency in Asia?

Has China’s renminbi unseated the Japanese yen as the new “safe haven” currency in Asia? Some market commentators have adopted this view given the renminbi’s recent strength, intensifying geopolitical tensions in Asia and Japan’s proximity to North Korea.

It’s true the renminbi has been the best-performing Asian currency this year¹, and it shares some hallmarks of currencies traditionally perceived as “safe havens,” but I’m not convinced. I believe the renminbi’s recent strength is less about investors viewing the currency as a stalwart in troubled times and more about policy changes from the People’s Bank of China (PBOC). I also don’t think the renminbi is of better “safe haven” status than the yen. Let’s take a more nuanced look at the currency:

The PBOC has taken steps to assert more control over the currency

In May, the PBOC introduced a new “countercyclical variable” to help reduce the renminbi’s short-term volatility versus the US dollar. This new countercyclical variable process reinforces Chinese authorities’ ability to influence the currency, adding another undisclosed variable on top of the prior day’s closing price to set the day’s benchmark.

This move was significant because it signaled the PBOC wanted to look through short-term gyrations in the renminbi that were inconsistent with what it deemed to be the currency’s ”fair value.” I interpreted this to imply that the PBOC felt the renminbi was back at a level more consistent with fair value after nearly two years of depreciation in real effective exchange rate (REER) terms. Simply, the PBOC was done allowing the renminbi to depreciate in REER terms. In my view, this policy change is the main reason behind the currency’s recent strength.

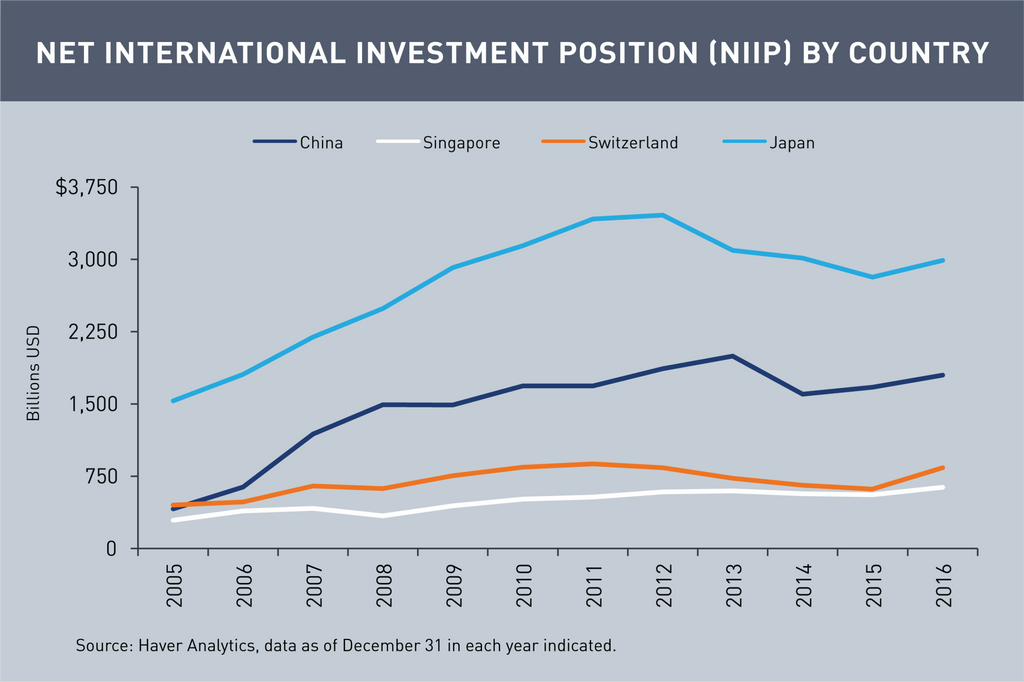

China’s net international investment surplus doesn’t qualify the currency as a “safe haven”

China has a sizable current net international investment position (NIIP) surplus, which makes it a net creditor to other countries. Currencies perceived as “safe havens” are generally associated with countries that have a NIIP surplus. During periods of risk aversion, countries with a NIIP surplus typically see their currencies appreciate as investors bring their foreign assets back home. This trend can raise the demand for the country’s currency.

China’s NIIP surplus is very large, satisfying the NIIP surplus condition of a relative “safe haven” currency, but its NIIP still remains significantly lower than Japan’s (Japan is the world’s largest creditor nation). More importantly, with partial capital controls still in place for the renminbi, it is hard to ascertain what the true value of the NIIP would be if the capital accounts were fully open. Until China allows real two-way free flow of capital, it is difficult to see the renminbi as a relative “safe haven” currency.

MALR020797

¹As of September 5, 2017.