Author

Why Insurance Companies Should Consider Emerging Market Corporate Debt

In this article, Dilawer Farazi, Co-Head of the Emerging Markets Debt Team, Portfolio Manager, addresses key reasons why emerging market (EM) corporate bonds make sense in an insurance company portfolio.

No matter how the capital markets gyrate, the imperative for insurance companies to deploy capital efficiently remains unchanged. The following article outlines why we believe EM corporate bonds, an often-underappreciated asset class, are a strategic source of income, diversification and relative value. For insurance companies navigating today’s environment, they offer a compelling way to balance yield objectives with prudent risk management.

A Positively Evolving Opportunity Set

A key starting point on the topic of emerging markets is that they should not be viewed as a single, uniform asset class. The opportunity set spans more than 55 countries, with wide dispersion in macro conditions, policy frameworks and credit fundamentals. For institutional investors, this breadth can create meaningful scope for selective allocation and diversification.

More broadly, the evolution of EM debt markets has been supported by improved economic architectures across many countries. Structural reforms—including more disciplined monetary policy, fiscal rules and inflation-targeting regimes—have strengthened policymakers’ ability to absorb shocks. In parallel, many countries have built more substantial foreign exchange reserves, while both sovereign and corporate issuers have increased access to local-currency funding. This has reduced reliance on US dollar financing and helped improve debt sustainability.

These developments have supported capital inflows, stronger domestic investment and, in many cases, better productivity and earnings outcomes. Combined with favorable demographic trends in parts of the EM universe, this has reinforced a relatively stronger growth backdrop. Notably, although the IMF’s April 2026 global growth report lowered its broader global outlook following the energy shock, it still projected EM growth of 3.9% in 2026, compared with 1.8% for developed markets.

Incorporating Hard-to-Forecast Risks in EM Portfolios

From our perspective, assessing EM in 2026 begins with fundamentals and their risk implications. That remains the foundation of our investment process. While forecasting disruption or volatility across regions may be intellectually engaging, we believe investors are generally better served by focusing on building resilient portfolios grounded in sound fundamentals and thoughtful risk assessment.

Across EM, these fundamentals have remained broadly robust through a range of geopolitical environments. In EM corporates, we believe that resilience—evident in 2025—has continued into 2026, supported by several factors:

- supply chain flexibility

- trade route optimization

- cost pressure pass-through

- increasing diversification across sectors within the opportunity set

In our view, a disciplined research and portfolio construction process can help investors capture this evolving opportunity set in a way that supports income, total return and diversification objectives. We seek to understand each country and issuer not only as they are today, but as they evolve over time. Working closely with our analysts, we aim to identify resilient credits with the potential to deliver attractive risk-adjusted returns despite volatility, while remaining mindful of downside risks, including ratings migration.

Relative Spreads and Compelling Opportunities

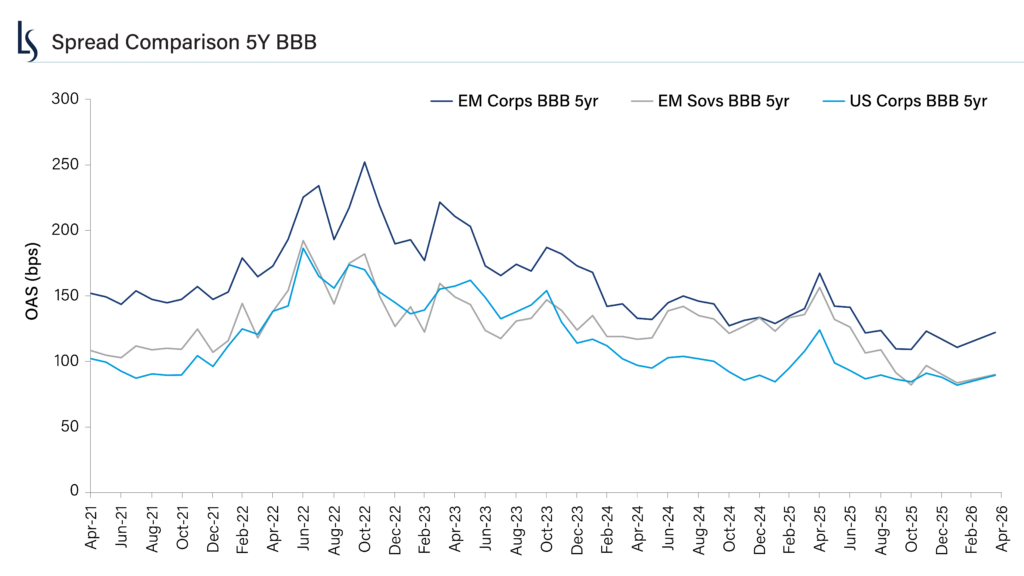

For an insurance company’s perspective, EM corporate spreads continue to compare favorably with developed market credit, offering potential incremental income without requiring a move materially down in quality. In investment grade, we continue to see a spread premium in A and BBB rated issuers relative to developed market peers, with valuations broadly in line with the three-year average and only modestly tighter versus the five-year average, which remains influenced by the post-COVID-19 dislocation.

OAS is option adjusted spread. Source: Loomis Sayles, as of March 30, 2026. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Indices are unmanaged and do not incur fees. It is not possible to invest directly into an index. Past performance is no guarantee of future results.

That relative value is notable at a time when elevated capital spending among some US investment grade issuers—particularly in technology—could pressure leverage metrics. By contrast, EM investment grade corporates have generally maintained lower net leverage and stronger interest coverage than developed market issuers. On a duration-adjusted basis, the BBB segment in EM corporates continues to stand out relative to both EM sovereigns and developed market sovereigns. In our view, that underscores the more compelling value in EM corporates for insurers seeking additional spread alongside resilient issuer fundamentals.

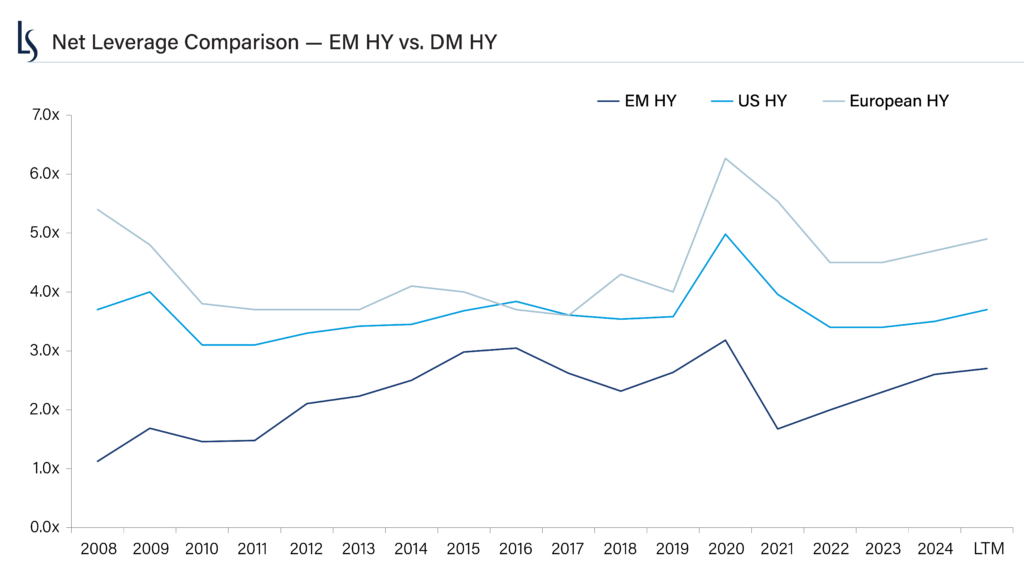

Within EM corporate high yield, spreads are currently tighter than their three-year and five-year averages, which reinforces the importance of issuer selection. EM sovereigns continue to offer limited pickup relative to developed market credit. EM corporate high yield issuers, in aggregate, continue to operate with leverage roughly one turn lower than US high yield corporates and two turns lower than European peers. For insurance portfolios that can support a selective allocation to EM high yield, we believe it is important to focus on credits with durable business models and manageable refinancing risk.

Loomis Sayles, as of March 31, 2026. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Indices are unmanaged and do not incur fees. It is not possible to invest directly into an index. Past performance is no guarantee of future results.

From a sector perspective, we see several areas that may be particularly relevant for insurers seeking a balance of income and resilience. In energy, we favor fundamentally stronger, lower-cost producers that we believe are better positioned to withstand commodity cycles. We also see opportunity in mining, where long-term demand for metals tied to AI-related infrastructure may provide structural support. Telecom remains attractive in our view because of its relatively predictable cash flows, demographic tailwinds, low data penetration and potential for deleveraging following periods of higher capital investment. Utilities with contracted off-take arrangements—often with government ownership—can also offer a combination of stability and visibility that may align well with insurance balance-sheet objectives. In addition, non-cyclical consumer issuers may benefit from the higher-growth profile present across many EM economies.

Our fundamental approach seeks to identify opportunities across these sectors and across regions including Asia, Emerging Europe, the Middle East, Africa and Latin America. Latin America currently offers some of the widest spreads across both investment grade and high yield issuers, although we remain attentive to idiosyncratic developments and an active electoral calendar. For insurance companies, we believe this breadth of opportunity can support diversified exposure across countries, sectors and rating bands, with the potential to enhance portfolio income while maintaining a disciplined focus on credit quality and downside risk.

Looking Forward

For insurance investors, EM corporate bonds may offer a compelling combination of incremental yield, resilient credit fundamentals and diversification. Across both investment grade and high yield, many EM issuers continue to demonstrate lower net leverage and higher interest coverage than similarly rated developed market peers, supporting a strong credit profile and relatively low default rates. In our view, these characteristics can make the asset class particularly relevant for insurers seeking attractive income with a disciplined focus on balance sheet strength and downside resilience.

Technical conditions also remain supportive. Many EM issuers have reduced reliance on external borrowing, benefited from deeper local-currency funding markets and prefunded near-term needs, contributing to limited net issuance. Against a backdrop of reinvestment demand, this constrained supply may continue to support valuations, in our view. With developed markets facing slower growth, higher debt burdens and policy uncertainty, EM corporates may offer insurers an opportunity to enhance portfolio yield while maintaining diversification across countries, sectors and issuers.

Disclosure

This marketing communication is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This information is subject to change at any time without notice.

Diversification does not ensure a profit or guarantee against a loss.

Commodities, interest and derivative trading involves substantial risk of loss.

Market conditions are extremely fluid and change frequently.

Indices are unmanaged and do not incur fees. It is not possible to invest directly in an index.

Any investment that has the possibility for profits also has the possibility of losses, including the loss of principal.

Past performance is no guarantee of future results.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

8971631.1.2

Author