Author

Corporate Health Outlook: Improvement Broadens as Expectations Rise

Our latest survey of Loomis Sayles credit research analysts showed that optimism is the highest it’s been in several quarters, with nearly all indicators moving in a positive direction. Importantly, the improvement is showing up in measures tied directly to profitability and balance sheet strength, suggesting that many companies are moving toward a healthier credit profile.

This improvement is unfolding against a backdrop of elevated expectations. Consensus earnings forecasts have been revised higher consistently, and both equity and credit markets are reflecting a broadly constructive view of the economic and corporate backdrop. As a result, we believe the hurdle for further upside has risen, even as the underlying fundamentals continue to strengthen.

About the CANDIs

Once a quarter, we survey Loomis Sayles’ credit research analysts to assess their bottom-up views of approximately 30 different industries. We quantify their responses using a proprietary tool known as the CANDIs—an acronym for Credit Analyst Diffusion Indices (click here to learn more). The process culminates in a forum that brings together our credit analysts and top-down global macro strategists to discuss the CANDIs’ output through the lens of the credit cycle. The results can be an indicator of how key corporate health metrics may trend over the next six months.

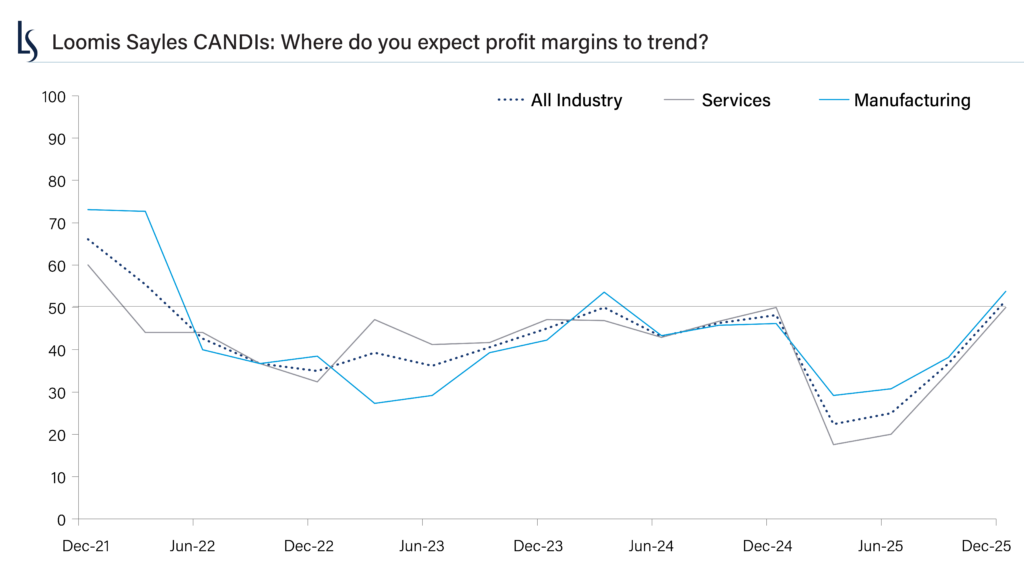

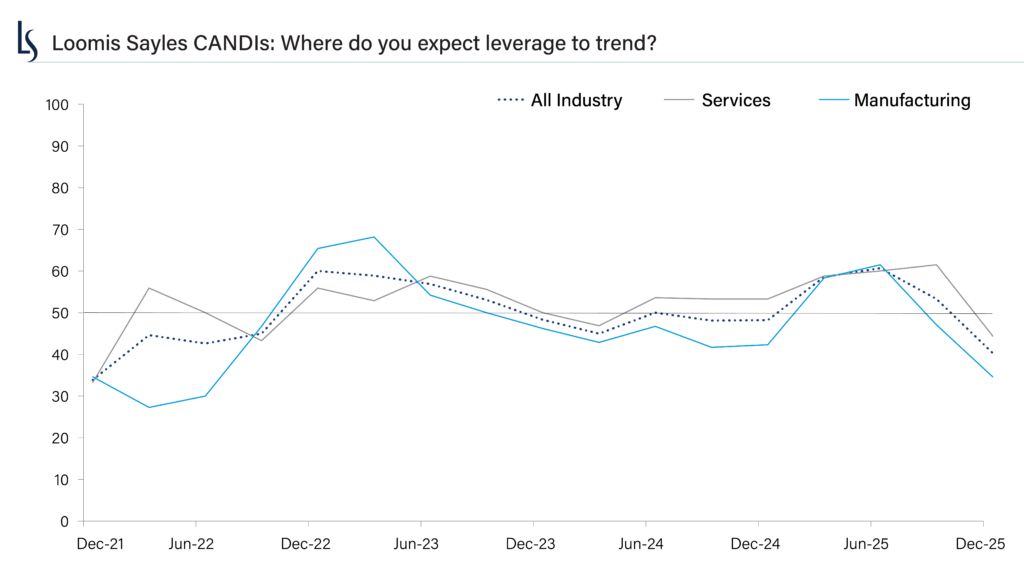

Margins strengthen as leverage declines

Perhaps the most consequential development in this quarter’s CANDIs survey is the combination of improving margin expectations and declining leverage. Expectations for profit margins rose sharply, indicating that our analysts expect a positive trend across services and manufacturing industries. Leverage expectations, meanwhile, fell to one of the lowest readings observed since the survey began, suggesting that leverage may trend lower.

Chart source: Loomis Sayles Credit Analyst Diffusion Indices, as of January 29, 2026. For the profit margins component, readings above 50 indicate a rising trend. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

This pairing should support credit quality, in our view. In manufacturing, margins appear positioned for modest expansion, while services-sector margins are expected to remain stable at elevated levels. Importantly, the improvement in profitability is occurring alongside balance sheet repair rather than being driven by increased borrowing.

Encouragingly, banks, which represent a significant portion of the broad credit indices, are also participating in the margin improvement, reinforcing the signal of broad-based fundamental strength.

Manufacturing shows resilience despite lingering cost pressures

Beneath the broad improvement, differences remain between manufacturing and services. Input and supply chain costs continue to weigh more heavily on manufacturing, reflecting residual tariff effects and exposure to imported materials. Services businesses benefit from a more domestically oriented cost structure and closer ties to US demand.

Despite those pressures, manufacturing fundamentals improved more decisively this quarter. Pricing power strengthened, margins improved and leverage declined more sharply than in services. In contrast, services-sector margins appear more stable than expanding, though they remain elevated.

This divergence suggests that manufacturing companies have been able to offset cost pressures through pricing discipline and productivity gains. In services, steadier demand from higher-income consumers has helped support profitability even as price sensitivity remains a consideration.

Strengthening fundamentals, greater expectations

The CANDIs results point to a stronger assessment of corporate health than in recent quarters. Corporate fundamentals are improving across a broad range of industries, supported by stronger margins, declining leverage and resilient earnings expectations. We believe these conditions are consistent with a cyclical expansion that remains supported by solid balance sheets.

Chart source: Loomis Sayles Credit Analyst Diffusion Indices, as of January 29, 2026. For the leverage component, readings above 50 signal a rising level of fundamental deterioration. The chart presented above is shown for illustrative purposes only. Some or all of the information on this chart may be dated, and, therefore, should not be the basis to purchase or sell any securities. The information is not intended to represent any actual portfolio. Information obtained from outside sources is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization.

At the same time, the environment has become more demanding. Consensus earnings expectations for 2026 and 2027 have been revised steadily higher over the past 18 months, and both equity and credit markets share a broadly bullish outlook. With incremental upside likely harder to achieve, modest disappointments could lead to periods of volatility even if the underlying fundamentals remain sound.

Valuations reinforce that dynamic. Credit risk premiums appear slim across much of the market, making it more challenging to aggressively add exposure to credit despite the positive outlook. In this setting, we think spread widening driven by modest fundamental misses may prove more constructive than destabilizing. If earnings and balance sheets remain generally intact, such episodes could create potential opportunities, in our view. Pockets of pressure remain in select areas such as autos and building products, where leverage and input costs warrant closer monitoring, but we believe these risks remain industry-specific rather than broadly systemic. Importantly, Federal Reserve policy flexibility can provide an additional buffer should conditions weaken materially.

Taken together, we see a clear message from the CANDIs survey. Corporate fundamentals are strengthening across a widening set of industries, but expectations are high and valuations leave less margin for error. In this environment, we believe discipline and selectivity may matter as much as the direction of corporate health itself.

8777571.1.1

Market conditions are extremely fluid and change frequently.

This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Information, including that obtained from outside sources, is believed to be correct, but Loomis Sayles cannot guarantee its accuracy. This material cannot be copied, reproduced or redistributed without authorization. This information is subject to change at any time without notice

Author